Executive Summary

In early March, the National People’s Congress in China set the country’s lowest growth target in 35 years, at less than 5 percent. Even that target can only be achieved by continuing the huge trade surplus that has driven economic growth since the collapse of a real estate bubble. This strategy was apparent in the trade statistics for the first two months of 2026, which showed exports growing at 22 percent. Last year’s trade surplus had already exceeded $1.2 trillion.

This report explores why China is locked into a slow growth pattern that is unsustainable without massively overproducing industrial goods, which overwhelms domestic consumption capacity. The state directs investment to subsidized industries in new technology sectors such as robotics, green energy, advanced manufacturing, and artificial intelligence. Because these favored industries compete with other advanced economies and are funded by a massive growth of debt, few resources are available to improve the primitive and undeveloped social welfare system. This—along with the loss of savings invested in the failing housing market, lack of private investor confidence, and rapid demographic decline—weakens domestic consumption. Apart from a narrow elite of wealthy entrepreneurs and Communist Party members, most Chinese people do not have adequate purchasing power to help stimulate economic growth. Meanwhile, Xi Jinping’s policy consistently favors investment in projects that seek to undermine the West’s leadership in technology and national power.

Falling tax revenues and low-to-negative returns on investment contribute to distressed balance sheets of central and local governments as well as in the state-dominated banking system. Chinese authorities have fostered huge increases in the money supply, partly to pay for rolling over or absorbing distressed debt. They also retain tight control over foreign currency earnings, international capital flows, and foreign exchange trading to keep narrow limits for the exchange value of the yuan. China has kept its currency even more undervalued relative to non-dollar currencies than to the dollar. Without its currency manipulation and capital controls, Beijing could not avoid the appreciation of the yuan, which would undermine its export-oriented trading system.

China effectively extracts needed savings from the Chinese people with its underfunded social welfare system and low returns on invested capital to fund its industrial policy goals, national defense buildup, and Chinese Communist Party apparatus. The United States and its allies could deflate the self-reinforcing bubble of this system by pushing back against Beijing’s mercantilist policies, for both imports and exports, and imposing sanctions for money laundering, including on bank officials implicated in such activities. Chinese banks contributing to currency manipulation could also be subject to penalties such as suspension from the dollar-based clearing system.

Introduction

Although most observers of the Chinese economy acknowledge that its era of rapid growth is behind it, there is a deep division between those who believe it will overcome its current problems and dominate the global economy, and those who see it as fatally flawed and headed for rapid decline. In some senses, though—as Desmond Shum astutely observes[1]—this is probably the wrong question to ask. Instead, the heart of the matter is, Who is harmed by the economic architecture of the current Chinese model, and is it sustainable?

A closer analysis has been emerging in recent years suggesting that, in fact, the most significant losers are the Chinese people, along with the industrial and market-oriented economies that have prospered in the United States–led economic order, loosely identified by labels such as “the Washington consensus.” This analysis is accurate, and furthermore, the structure of the Chinese economy is more vulnerable than many analysts care to admit to countermeasures from the countries that are being harmed by what can be called “Chinese mercantilism.”

Perhaps less widely understood and appreciated is that the deprivations visited on the Chinese people by the rigid, export-driven, and centralized economic structure perfected by Chairman Xi Jinping since 2012 have left the People’s Republic of China (PRC) vulnerable. If the Chinese Communist Party (CCP) fails to change course, and if the targets of Chinese mercantilism and the accompanying political and military pressure resist the Xi regime’s economic aggression, it might be possible to effectively challenge its iron rule and uncompromising stance. The key is understanding the structure and functioning of China’s financial system.

How the Chinese Economy Works

Most China observers now concede that exports are the most important driver of China’s growth, along with some contributions from the persistent overinvestment in infrastructure and favored industries including steel, artificial intelligence (AI), and green technologies. The corollary is that various domestic policies supporting China’s manufacturing and technology sector feed the export engine by stimulating overproduction.[2] Even though the International Monetary Fund (IMF) and the World Bank are constrained by the requirement to use official Chinese data in their analyses of the country’s economy, both have concluded in recent years that the Middle Kingdom is too reliant on exports.

Beijing’s domestic policies also promote a savings-oriented economy, which in turn reinforces the need to flood the world with excess production. Both institutions have long urged policymakers in China to move in the direction of stimulating consumption to steer the economy away from an export-driven model.[3] Xi and his government, by overwhelming the world with Chinese exports and stifling attempts to improve the social safety net supporting the Chinese people, have consistently resisted any meaningful shift toward consumption to drive the economy.

Finding evidence for this is difficult, as Substack blogger Michael Nicoletos[4] has noted. In a recent post, he explained, “Finding the real story about China takes work. The numbers exist. . . . But [they are] scattered.” The Rhodium Group, one of the best archaeologists of Chinese data, has carefully documented the economic reality behind the unreliable statistics offered, without evident humility, by Chinese statisticians. Overall growth is closer to 2 percent than the official figure of 5 percent, and the path to acceleration is highly constrained.[5]

Household consumption growth in China has slowed in recent years and remains below 40 percent of total gross domestic product (GDP), far behind the 68 percent figure for the consumer-driven US economy and the mid-50 percent figures in the European Union and Japan. In 1949, 49 percent of GDP in the new PRC was accounted for by consumption.

One important reason for the dearth of consumption is the collapse of the property sector in the last decade. Prior to its collapse, starting in 2001, this sector represented about 60 to 70 percent of household wealth. Some 70 million housing units now sit unsold or partially finished, many already paid for by Chinese families, since the sector collapsed.[6] Housing prices fell by one-third prior to early 2025 and continue to decline. The former head of China’s National Bureau of Statistics estimated that some $5.8 trillion (40 trillion yuan) of household wealth was destroyed in the property crash, and the situation is still deteriorating.[7] It will take many years to recover from the crash, as it did in Japan in the 1980s, due in no small part to the reverse wealth effect of the crash.

Chairman Xi is striving to overcome the US-led economic order and undermine US and Western economic leadership through programs such as Made in China 2025 and the Belt and Road Initiative (BRI). As part of this drive, Xi has maintained an investment-led policy of allocating capital to those programs, as well as to favored industries that often have unprofitable business models. This tends to drain resources that could be used to promote the well-being of Chinese workers and families.

A problem with this strategy, increasingly coming into focus, is that the investment program is less and less efficient in providing economic returns. Millions of housing units sit empty due to overproduction, and because available capital is relentlessly channeled to infrastructure and industry, there are beautiful high-speed train networks that are but sparsely used by paying customers, outside a few heavily used corridors. China continues to build massive water projects such as the Great Bend Dam, which will have three times the generating power of the Three Gorges project.[8] This is a dangerous hydroelectric project on Sino-Indian borderlands with some of the world’s highest propensity for seismic events. Such initiatives promote jobs and spending in the short run but destroy ancient villages and monasteries and upset ecological balances. These types of prestige projects seldom generate reasonable returns on investment while destroying traditional landscapes and ways of life.

Both productivity and capital output ratios (returns on invested capital) have declined in recent years due to the shift toward favoring bank loans for state-owned enterprises (SOEs), infrastructure project developers, and favored industrial sectors.[9] A recent IMF working paper calculated that since Xi came to power, up to 4.4 percent of GDP has consisted of subsidies to industry,[10] which is three times the level of subsidies in the EU, with its industry-friendly policies. Beijing continues to approve projects for infrastructure, energy independence, and AI capabilities no matter what the expected economic return.

The shift in lending to favor SOEs also deprives the more productive private sector of needed funding. Growth in loans to households, according to Logan Wright has “collapsed” from a high of over 10 percent of GDP before the COVID crisis to less than 1 percent of GDP in 2025. The household category, importantly, includes sole proprietorships, which in the fast-paced growth years were an important source of growth in the services sector as well as housing.[11]

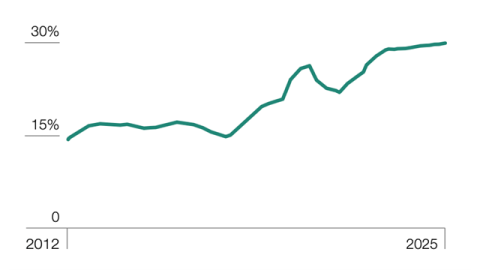

The more productive new services sectors, especially private firms, are being systematically deprived of bank loans by the PRC-directed economy. While money-losing SOEs saw their profits fall by 4 percent last year, private sector profits fell by only 0.1 percent, and profits from foreign-owned enterprises grew by 4.2 percent. One-third of all firms in China lost money in recent years (see figure 1).[12] Last year, large banks experienced their lowest profitability since 2007, and non-performing loans continue to increase.[13] This is due in part to banks being directed to lend to SOEs and other money-losing firms as part of Beijing’s drive to develop new industries and preserve social stability.

Figure 1. Share of Chinese Entities Operating at a Loss, Rolling 12-Month Average

Source: “China Bulletin: March 4, 2026,” US-China Economic and Security Review Commission, March 4, 2026, https://www.uscc.gov/trade-bulletins/china-bulletin-march-4-2026.

For all these reasons, and because of the difficulties of operating in China, investments by foreign firms, especially those in the US and Europe, have declined significantly in the last few years. While in the high-growth years of the 1990s and 2000s, Beijing could count on expanding Western direct investments and portfolio investments, China’s poor economic performance, especially since COVID and growing trade restrictions in response to Chinese mercantilism, has reversed the trend.[14]

Compounding the problem of declining growth and capital productivity is the loss of household purchasing power because the PRC is unwilling to devote resources to the social welfare system. Constraints on government finances have been a major factor in exacerbating this problem in recent years. Tax revenues hovering around 17 percent of the economy are much below average for developed and even developing economies. Total government revenues in China, at about 26 percent of GDP, lag behind expenditures by developed countries and even developing countries such as Mexico and Colombia. Revenues from land sales have plummeted, and general tax revenues have declined in recent years due to the slowing economy, the collapse in real estate values, and the lack of new development.[15]

Chairman Xi has consistently favored generous financing for manufacturing, technology, and infrastructure, and for the CCP’s privileged 100 million members, over building an adequate social welfare system. Unemployment benefits cover only about 47 percent of the urban labor force and even less of the largely unskilled rural labor force, and benefits for covered urban workers amount to less than 20 percent of average wages.[16] Retirement payments for the largest pension program start at only a bit over $20 per month.[17] A survey of large operating firms in 2024 also showed that only 28 percent were fully compliant with their social welfare obligations, despite pressure from Beijing and a ruling from China’s top court in 2025 mandating full compliance.[18]

Health care is an even heavier burden for Chinese families.[19] Although theoretically, two-thirds of the population is covered by the medical system, hundreds of millions lack coverage. The personal contributions required for coverage have grown by 38 times since 2003, and tens of millions—25 million in 2023 alone—have dropped out of the system altogether.[20] The system is so underfunded and coverage is so restricted that citizens, especially in rural areas and in services sectors, are forced to self-insure or try to buy private insurance.

In an earlier paper, this author and a colleague, Alexander Aibel, provided more detail on the weakness of China’s social safety net, offering evidence that the system is causing some loss of confidence in the future among the general population and widespread but isolated protests against government authorities. There is also dissatisfaction with the financial institutions that allocate capital, persist in demanding repayment of mortgages even for undelivered housing units, and provide low returns on savings and investment.[21] It is also common for government employees and contractors to be paid late or not at all, especially by beleaguered local governments.[22]

The combination of a lack of state welfare support, stagnant wages, and these other problems goes far to explain the high propensity to save in China, where average family savings hover around 32 percent of GDP, compared with around 5 percent of GDP in the United States. In the coming years, reductions in workforce size, the collapse of the birth and marriage rates, and the concomitant need to support elderly family members make a reversal in the tendency to save highly unlikely.

Deferred consumption also contributes to the current deflation. A self-reinforcing cycle of constrained consumption growth and deflation reinforces the dynamic, which undermines domestic-led growth and helps build reliance on exports. Nicoletos cites projections of population decline in China between 640 and 775 million by 2100. If current trends continue, the dependency ratio would increase from about 4 workers per retiree to 1.2 to 2 per retiree.[23] Unless robots can take over a significant number of jobs, this would of course deal a severe blow to growth goals.

Finally, the massive concentration of wealth in China, where 93 percent of the population has $3,340 or less in net assets, is another key factor in weak consumption. Official Chinese sources estimate the Gini coefficient at 0.474, well above that of developed countries, where it ranges from 0.24 to 0.36.[24]

Growing Debt, Monetary Easing, and the Dangers of Financial Crisis

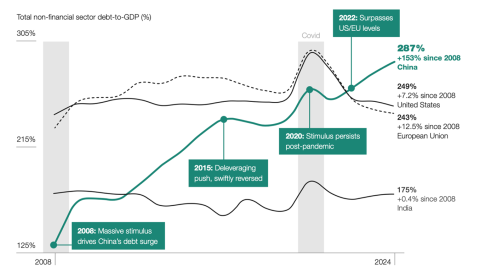

Chinese responses to the great financial crisis and COVID, along with slowing growth and massive subsidization of the industrial sector, have caused a huge increase in both public and private debt (see figure 2). According to the IMF, total social financing, which includes both public and private debt, is well over 300 percent of GDP. The IMF estimates that private debt surged by 17 percent annually after 2021. It also estimates that the total budget deficit in 2025 will be 14 percent of GDP and that the deficits will continue at double-digit rates for the next few years.[25] Much of the debt is hidden and difficult to account for, but according to the IMF, the financial problems of local governments are “combustible,” and it recommends a diet of higher taxes and tolerating bank insolvencies to reduce it. Deflation is making the cost of amortizing debt much higher as time goes on.[26]

Figure 2. China Has Taken on More Debt Than Any Other Major Economy Since 2008

Source: “No, China Is Not the Adult in the Room,” Bullionbite, Substack, November 23, 2025, https://www.bullionbite.com/p/no-china-is-not-the-adult-in-the.

Chinese banks are consistently encouraged to extend (and “pretend”) the terms of distressed loans to SOEs and favored private firms to avoid social unrest from unemployment and from government failure to provide adequate basic services. This adds to the impact on the banking sector and increases the need to offload goods produced by “zombie” manufacturing firms to international markets. Households holding accounts in distressed banks are at risk of losing their savings and competitive income, which gives authorities an incentive to avoid social unrest by subsidizing the banks.[27]

Perhaps a more serious problem is that Beijing is being forced by the rapidly declining rate of return on capital investment to devote an increasing portion of lending to recapitalize and subsidize both banks and firms operating at a loss. Net interest margins have declined by half since 2014. As a result, loans to the real economy have fallen by 9 percent of new credit creation in recent years. Much of the gap is likely going into propping up the banking sector instead of to new investment.[28]

In recent years it has also become evident that China is printing money and manipulating the value of its currency as one way to address its debt problems. Currency manipulation permits Beijing to control the macroeconomic effects of monetary policy and protect its ability to export its way to growth. China tightly controls the yuan-dollar exchange rate, which allows it, among other things, to retain competitive purchasing power for commodities such as metals, grains, fossil fuels, and high-tech goods like advanced semiconductors and jet engines, which are generally priced in dollars. This strategy also contributes to China’s long-term goal to position the yuan as a competitor to the dollar for foreign reserves in third countries.

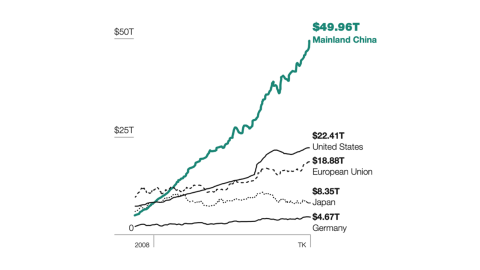

Less well understood is that for decades, China has been creating money, equivalent to the US M2, at a scale much in excess of its domestic economy’s growth needs (see figure 3). In 2025 it printed some $4.5 trillion worth of yuan while its economy grew by a little bit less than $700 billion.[29] Since 2000 the money supply in China has grown six times faster than in the United States, even though its economy remains at least a third smaller than that of its largest competitor.[30] Since 2020 China’s M1 and M2 have grown by 116 percent and 72 percent, respectively. It now swims in more monetary stock than the US and EU combined.[31]

Figure 3. M2 Money Supply in China and Other Countries

Source: Ronnie Khoo, “China M2 money supply just hit a new all time high of ¥326.13 trillion,” Facebook, April 16, 2025, 11:51 a.m., https://www.facebook.com/ronniekhoo82/posts/-china-m2-money-supply-just-hit-a-new-all-time-high-of-32613-trillionin-both-201/10162726272696108/.

Monetary growth is controlled by the PRC, which also directs and allocates bank lending. China’s total debt has grown by some 15 percent annually in the twenty-first century. A plausible explanation of such excessive growth is that Beijing is creating an excess money supply to promote growth in its faltering economy. The IMF estimates that since Xi came to power, annual subsidies for industrial policy have been 4.4 percent of GDP. This policy includes cash subsidies, tax benefits, land subsidies, and subsidized credit. The government-owned banking sector itself has been recapitalized several times. As noted earlier, the banking sector is facing increasing challenges in part because Beijing forces it to support failing local governments and roll over both government and distressed private sector debt.

Another drain on Chinese finances is that the need to keep the BRI liquid also requires liquid resources from the banking sector, which originates most loans for this program. Almost all aid to BRI companies is in the form of loans. Between 60 and 80 percent of all BRI loans are to countries in financial distress, and since 2008, some $250 billion in non-performing loans have been recognized among recipients.[32] As noted earlier, a substantial portion of SOEs lose money and require regular injections of capital. All too often, the Chinese model of competition among public and private firms to build new manufacturing industries results in many failed enterprises and loans that are written off or hidden in opaque local and regional government balance sheets.

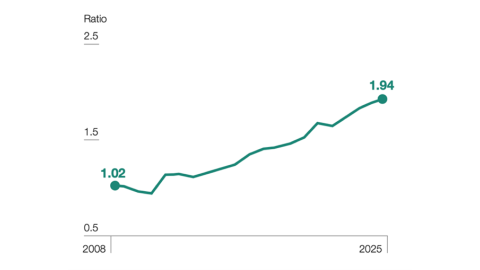

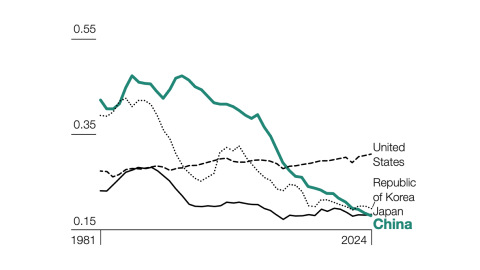

A primary effect of multiple inefficiencies in the Chinese growth model is that the lending required for each dollar of incremental growth has doubled in the twenty-first century (see figure 4).[33] Productivity improvements have not compensated for the decline in capital efficiency. Figure 5 compares Chinese capital efficiency over several decades with the United States and other competitors. It shows a steady decline in this indicator for China while the United States has steadily improved. The Chinese ratio now approximates that of Japan, which has been mired in stagnation for decades.

Figure 4. Ratio of Bank Loans to GDP in China

Source: Derek Scissors, “When Does China Stop Growing (Entirely)?,” American Enterprise Institute, March 5, 2026, https://www.aei.org/research-products/report/when-does-china-stop-growing-entirely/.

Figure 5. Capital Efficiency Ratio

Source: Mike Bird (@Birdyword), “Nice piece here from @BrianSpegele. China is a big victim of Chinese overinvestment! Latest Penn World Tables show that by 2023 Chinese capital efficiency below even Japan's, and far below the US level, despite still being much poorer than either,” X, December 23, 2025, 1:20 p.m., https://x.com/Birdyword/status/2003531133586407496.

In a market economy, such extravagant growth in the money supply and government debt would normally have some impact on inflation and the value of the currency. However, in China the chronic outsized trade surplus helps blunt, to a large extent, the impact on inflation and especially on the value of the currency. China maintains rigid capital controls, limiting outflows of capital and maintaining a tight grip on dollars and other foreign currencies held in the country. Nearly all foreign currency earned in mercantilist China, with its trade surplus of over $1 trillion in recent years, is required to be sold to the People’s Bank of China (PBOC). Some exceptions are made, however, for the operating needs of trading firms. China also restricts trading in foreign currencies to the PBOC and the Hong Kong Shanghai Bank, whose actions Beijing keeps under tight control. Thus, the central government keeps a lid on foreign currency outflows, which might affect its ability to maintain the narrow range of the yuan’s exchange rate against the dollar. With such a consistent and massive trade surplus, normal economics would predict a much higher value of the yuan. Given the propensity of the Chinese to seek to move currency out of the country, without this tool, Beijing would lack the ability to control exchange rates and prevent possible pressures on bank liquidity.

Many knowledgeable analysts now concede that the yuan is significantly undervalued.[34] While it has marginally increased its value against the dollar in the last 18 months or so, it has weakened significantly against other currencies. Manipulating the yuan helps Beijing manage its trade surplus with the US while offsetting recent declines by increasing trade surpluses with the eurozone, Southeast Asia, Africa, and South America. The disparity with the eurozone is especially striking, as the euro has appreciated against the yuan by some 40 percent since COVID, doing considerable damage to industrial centers in the heart of Europe. Germany’s trade deficit with China is now 3.6 times greater than in 2020, and the deficit of the EU with other countries, including China, has doubled.[35]

Beijing, in short, can sustain currency undervaluation against most currencies but maintain stability with its main competitor, the United States, whose dollar is the global reserve currency. It engineers this fine-tuning through control of both capital movements and all foreign currency earned by Chinese firms, a tool it considers the linchpin of macroeconomic stability in China.[36] Given the dangers of capital flight, often articulated by analysts, this may indeed be the case.

One part of this strategy is for state banks to accumulate foreign assets in excess of current account balances. Brad Setser estimates that Chinese outflows of foreign currencies have been around $300 billion less than inflows per year. This difference results in the state banks making huge purchases of foreign notes, bonds, and other assets. He notes that this could be considered a form of “backdoor currency manipulation.”

In effect the PBOC and large “policy banks” are required to hold huge foreign exchange positions in relatively low-return assets such as bonds and notes from the US and other countries. If other parts of the banking system serving the domestic economy also have low or negative returns, as is the case in China, capital available for productive investment will be reduced and much will simply be destroyed. Setser notes that this is unsustainable under normal market conditions.[37]

It is worth noting that when China joined the World Trade Organization (WTO) in 2001, it promised to give national treatment, including trading in foreign currencies, to all foreign banks after a five-year “transition period.” Like many other commitments from 2001, this one awaits fulfillment, and many foreign banks and financial institutions have abandoned hope in the promise of participating in China’s vast financial markets.

The Self-Reinforcing Structure of Chinese Mercantilism

Desmond Shum, author of Red Roulette, who lives in the West after helping make fortunes in Chinese real estate, notes that the average Chinese worker labors almost 49 hours each week but that only 2.5 percent of Chinese workers achieve an average per capita income of $13,106 a year, or around $1,100 a month. He also points out that some 547 million Chinese live on less than $145 a month.[38] Analyst Derek Scissors calculates that average per capita disposable personal income is at $6,200 per year or about $1,216 per month.[39]

Xi is remarkably indifferent to the purchasing power and financial comfort of the Chinese laborer or retiree; when challenged with suggestions that he prioritize conditions for average families, he advises his compatriots to learn and appreciate the benefits of “eating bitterness.” His father, who according to Xi’s biographer Joseph Torigian is Xi’s inspiration and role model, also favored the needs of the CCP and the state over that of individuals. As Torigian notes, “Xi [Zhongxun] was comfortable with policy flexibility, but he was sensitive to the importance of justifying such innovations with ideological explanations, and he found consumerism and materialism deeply distasteful.”[40]

Indeed, the purpose and structure of the Chinese economy is to preserve the power of the CCP, position the nation as a leading global power, and promote economic growth based not on consumer welfare but on increasing manufacturing output, developing technology, and building modern infrastructure. The subsidies for these investment pillars, their expansion through competition between city and provincial governments to meet Beijing’s goals, and political competition of the cadres in these local institutions promote overproduction and make exports necessary to clear overproduction.

The well-being of individuals and families takes a poor second place to industrial growth and infrastructure development. Funds needed to balance the economy more toward domestic consumption are simply not available because state firms are not profitable, government revenues are constrained, and state and local governments have high levels of debt. Consumer wealth is also crippled by stagnating wages, the destruction of savings and assets in the property market crash, and the relatively undervalued currency, which limits imports and competitive pricing for goods and services inside China.

As has been the case throughout Chinese history, state power is built on the backs of the Chinese people. It is shared with a narrow elite of party members and firms favored in the CCP’s drive to dominate the global economy.

Responses to Chinese Mercantilism

The export-oriented Chinese economy and the CCP’s drive for technological dominance inflict considerable damage on market-oriented Western economies, but they also carry the seeds of effective countermeasures if the market economies can muster the political will to take collective action. China’s growth model is already being eroded by demographic decline, dependence on imports of raw materials such as fossil fuels and food, and deteriorating public and private finances. Its flooding of global markets to fund the subsidized industrial sector is generating growing global resistance to the import of goods such as electric vehicles, rare earths, green energy products, steel and aluminum, and consumer goods.[41] Even the EU,[42] India, and Southeast Asian countries are chafing at Chinese mercantilism. They are therefore willing, despite President Donald Trump’s erratic and costly threats, to reach “rebalancing trade deals” with him and his team.

China’s growing assertiveness, which supports rogue authoritarian states such as Russia and Iran and is backed by massive military expansion in the South China Sea and the first Pacific island chain, adds to the new awareness of erstwhile US allies that China is a political and economic threat. Market-oriented powers are now more widely accepting of resistance through tariffs and sanctions, such as those on Chinese oil imports from authoritarian states, sales of subsidized steel and electric vehicles, or military-related sales to Russia. Simply by making it more difficult for China to export and invest in unneeded infrastructure to sustain prosperity, they can continue to make Xi’s rigid mercantilist path more problematic for him in the future.

Additionally, not only has China systematically violated the principles of reciprocity and most-favored nation treatment embedded in the global trading system; it has long been a free rider in the global financial system, benefiting from asymmetrical access to the Western-dominated financial system that allows it to sustain its trade surplus. It also raises funds to finance domestic investment from the well-functioning, Western-dominated capital markets while its own financial markets are among the most protected in the world. The PRC systematically refuses to honor commitments to allow competition from Western financial services firms, which were a major part of its deal to join the WTO 26 years ago.

China also abuses the global financial system in tolerating, and even promoting, money laundering as part of its drive to weaken the West. Money laundering facilitates illicit and damaging activities such as the global drug trade, and enables Russia and Iran to sidestep Western sanctions on their fossil fuel sales and illicit weapons trading.[43]

Beijing’s currency manipulation is facilitated by the closed capital account. It is an especially egregious violation of China’s commitment to the West when it joined the postwar trade and financial systems. Many think that if China lacked the ability to prevent the free flow of capital and to limit foreign currency trading, capital outflows from the country could seriously undermine the stability of its banking system.[44] As noted earlier, the lack of confidence of foreign firms is one source of potential capital flight. But the principal danger is from Chinese private firms and individuals whose confidence in the economy is waning as growth slows, Xi cracks down on the private sector, and families are increasingly burdened by stagnation in social welfare benefits.

If President Trump is serious about undoing the damage from Chinese mercantilism and financial manipulation, he will work with traditional allies to pressure China to end its harmful practices. He has already deployed tariffs to blunt China’s mercantilism and sanctions to undermine its support for the axis of authoritarianism. This axis is now being weakened as the United States has arrested Nicolás Maduro of Venezuela, with Israel killed Ayatollah Ali Khamani of Iran, and weakened the economies of both those countries along with those of Cuba, Syria, and North Korea. The US could go further by demanding that China honor its WTO commitments on opening financial services. If Beijing simply allowed foreign financial firms to trade in foreign currencies in the Chinese market, capital flows and the PRC’s ability to keep its currency at levels most favorable to its trade policy would dramatically change. Trump can also work to gain support from allies—who are equally harmed by Chinese mercantilism and currency manipulation—to challenge Xi’s program.

Is it unreasonable to expect that currency values will reflect China’s persistent and gaping trade surpluses, which would typically lead to a stronger currency and thus enhanced purchasing power for long-suffering consumers?

Absent a change in Beijing’s policies, further trade restrictions to limit its mercantilist growth approach are in order. If Western financial firms were able to operate in China, this would improve the management and growth tools available to the broad public and contribute to building a better working alliance with market economies to limit Chinese mercantilism.

The United States could deploy tougher measures as well, such as labeling China a currency manipulator, hopefully with support from allies, and enforcing sanctions contemplated in the enabling laws. US law explicitly singles out delisting of Chinese firms from US stock exchanges, countervailing duties, and higher tariffs as responses to currency manipulation.

Because of China’s blatant violations of money-laundering regulations and Western sanctions on Russia, Iran, and Venezuela, there is ample justification for even tougher sanctions on individuals, banks, or entire jurisdictions involved in these practices. Section 311 of the Patriot Act authorizes sanctions and restrictions across entire jurisdictions. It contemplates prohibiting the targeted bank or financial institution from any dealings with the dominant Western banking system. That is, it could target a territory such as Hong Kong or an institution such as the PBOC with actions to exclude the targeted banks or territories from the Society for Worldwide Interbank Financial Telecommunication (SWIFT) and Clearing House Interbank Payment System (CHIPS) financial networks. This would have serious consequences for Chinese firms trading with the West as they could not use the dollar-based payments system that accounts for over half of global trade. It would also gut the Chinese effort to undermine the US-dominated global payments system. US law also allows criminal and civil penalties for individuals convicted of money laundering, or other requirements for secrecy and compliance under Section 311 and bank secrecy regulations.[45]

Concluding Remarks

Stronger measures against China’s closed financial system, such as those discussed above—along with coordinated tariffs and other penalties for China’s deeply embedded, highly subsidized mercantilist system—would seriously harm the PRC’s economic model. The only realistic path to sustained growth in China would be to adopt the changes suggested for many years by the IMF, the World Bank, and numerous economists, and to pivot toward broader consumer strength and less industrial subsidization and overproduction. Improved purchasing power from a properly valued currency and a more robust social welfare pension system are both keys to a realistic transition away from the PRC’s longstanding economic structure. Surveys of consumer confidence in China suggest acute discontent due to the multiple problems of consumer welfare and even despair at the lack of response from the CCP. Between the start of COVID in 2019 and 2024, consumer confidence cratered from a level of 125 to 80, where 100 is deemed confident.[46]

It is an open question whether concerted Western pressure in the form of trade restrictions and sanctions on China’s financial system, along with the deprivations the Chinese people suffer from Xi’s social and consumer welfare policies, can motivate him to change direction.

The other unanswered question is whether President Trump will adopt the actions suggested in this paper and elsewhere and confront Xi in a much more concerted fashion coordinated with market-oriented allies.

The jury is still out. Unfortunately, experience since Trump returned to office indicates that the impact of Chinese mercantilism and Beijing’s attempt to upend US world leadership may have to grow further to seriously motivate the president to confront Xi. And the Chinese leader himself has sufficient personal and familial experience with “eating bitterness” to make major changes difficult to achieve. But concerted Western action would test his staying power as popular discontent—along with the possible alienation of party elites and cadres due to declining growth and vastly increasing corruption purges—takes a toll.

- Desmond Shum (@DesmondShum), “China’s Prosperity: Built by Households, Claimed by the State,” X, February 11, 2026, 4:28 p.m., https://x.com/DesmondShum/status/2021697858202718625. ↑

- See International Monetary Fund, “IMF Board Concludes 2025 Article IV Consultation with China,” News Release, February 18, 2026, https://www.imf.org/en/news/articles/2026/02/18/pr-26053-china-imf-executive-board-concludes-2025-article-iv-consultation; Daniel H. Rosen, Logan Wright, Oliver Melton, and Jeremy Smith, “China’s Economy: Rightsizing 2025, Looking Ahead to 2026,” Rhodium Group, December 22, 2025, https://rhg.com/research/chinas-economy-rightsizing-2025-looking-ahead-to-2026/; and Logan Wright, “China’s Financial and Fiscal Decay,” Rhodium Group, February 19, 2026, https://rhg.com/research/chinas-financial-and-fiscal-decay/. ↑

- People’s Republic of China: 2024 Article IV Consultation-Press Release; Staff Report; and Statement by the Executive Director for the People’s Republic of China (International Monetary Fund, August 2, 2024), https://doi.org/10.5089/9798400284281.002. See also Unlocking Consumption: China Economic Update (World Bank Group, June 2025), https://openknowledge.worldbank.org/server/api/core/bitstreams/43f4bc2c-b457-4a6f-911f-8ad3bded0de9/content. ↑

- Michael Nicoletos, “The Elephant No One Wants to See: Why the World Ignores China’s Economic Crisis,” Michael’s Publications, Substack, January 25, 2026, https://michaelnicoletos.substack.com/p/the-elephant-no-one-wants-to-see. ↑

- Rosen et al., “China’s Economy.” See also Endeavour Tian, Logan Wright and Allen Feng, “China’s “New” Strategic Industries Will Not Produce 5% GDP Growth,” Rhodium Group, January 12, 2026, https://rhg.com/research/chinas-new-strategic-industries-will-not-produce-5-gdp-growth/. ↑

- P.K. Balachandran, “‘Ghost Towns’ Became the Face of China after Housing Sector Collapse,” Counterpoint, March 20, 2025, https://counterpoint.lk/ghost-towns-became-the-face-of-china-after-housing-sector-collapse/. ↑

- Qiu Xiaohua, “邱晓华:房地产深度调整与发展前景 | 观点年度论坛演讲” [In-depth adjustment and development prospects of the real estate market], Annual Forum Speech, March 20, 2025, https://www.163.com/dy/article/JR3TCV1L0519D45U.html. ↑

- Thomas Duesterberg, “The Dangers of China’s Megadam,” January 2, 2025, Wall Street Journal, https://www.wsj.com/opinion/the-dangers-of-chinas-planned-megadam-border-dispute-humanitarian-environmental-risks-e0c2312a. ↑

- Logan Wright, Grasping Shadows: The Politics of China’s Deleveraging Campaign (Center for Strategic and International Studies, April 2023), https://csis-website-prod.s3.amazonaws.com/s3fs-public/2023-04/230410_Wright_Grasping_Shadows.pdf?VersionId=23lg65zaQBlbwAKPTSQWtCxDaABjds7E, 16. ↑

- Daniel Garcia-Macia, Siddharth Kothari, and Yifan Tao, “Industrial Policy in China: Quantification and Impact on Misallocation,” Working Paper, International Monetary Fund, August 2025, https://www.imf.org/-/media/files/publications/wp/2025/english/wpiea2025155-source-pdf.pdf. ↑

- Wright, “Fiscal Decay,” 3. ↑

- People’s Republic of China: 2024 Article IV Consultation. On profits see, 2025 Report to Congress (US-China Economic and Security Review Commission, November 2025), https://www.uscc.gov/sites/default/files/2025-11/2025_Annual_Report_to_Congress.pdf, 42; and China Bulletin (US-China Economic and Security Review Commission, March 4, 2026), https://www.uscc.gov/trade-bulletins/china-bulletin-march-4-2026. ↑

- Kensaku Ihara and Kentaro Shiozaki, “China’s Biggest Banks Under Pressure as Trade War Heats Up,” Nikkei Asia, April 12, 2025, https://asia.nikkei.com/business/markets/china-debt-crunch/china-s-biggest-banks-under-pressure-as-trade-war-heats-up; and China Bulletin. ↑

- See Yoko Kubota and Liza Lin, “Western Firms That Flocked to China Are Now Pulling Back,” Wall Street Journal, September 11, 2024, https://www.wsj.com/world/china/western-firms-that-flocked-to-china-are-now-pulling-back-ea2f3c27; and Spencer Feingold, “US Companies Cut Investments in China to Record Lows. Here’s Why,” World Economic Forum, July 20, 2025, https://www.weforum.org/stories/2025/07/tariff-impacts-us-companies-cut-investments-china-record-lows/. ↑

- People’s Republic of China: 2024 Article IV Consultation, 3. ↑

- Unlocking Consumption, 32. ↑

- Unlocking Consumption, 11. ↑

- “China Faces Pivotal Welfare Reform Test as Court Ruling Hits Jobs, Small Firms,” Reuters, August 20, 2025, https://www.reuters.com/sustainability/sustainable-finance-reporting/china-faces-pivotal-welfare-reform-test-court-ruling-hits-jobs-small-firms-2025-08-20/. ↑

- Yanzhong Huang, “China’s Emerging Welfare Crisis,” Think Global Health, March 28, 2024, https://www.thinkglobalhealth.org/article/chinas-emerging-welfare-crisis. ↑

- Huang, “China’s Emerging Welfare Crisis.” ↑

- Thomas J. Duesterberg and Alexander Aibel, “How Weakness in the Social Safety Net Undermines the Political Compact in China,” Hudson Institute, December 9, 2024, https://www.hudson.org/economics/how-weakness-social-safety-net-undermines-political-compact-china-thomas-duesterberg-alexander-aibel. ↑

- Qian Zhou, “Labor Trends and Risk Management in China 2026 – New Publication Out,” China Briefing, March 3, 2026, https://www.china-briefing.com/news/labor-trends-and-risk-management-in-china-2026/. ↑

- Nicoletos, “The Elephant No One Wants to See.” Nicoletos cites estimates of population decline from the UN and demographer Yi Fuxian. ↑

- Figures are from “中金2023年中国财富报告” [2023 China wealth report], Zhihu, November 24, 2023, https://zhuanlan.zhihu.com/p/668579074. But the World Bank lists the PRC Gini coefficient as 0.36 in 2022. See “Income Inequality: Gini Coefficient: World Bank,” Our World in Data, accessed March 13, 2026, https://ourworldindata.org/grapher/economic-inequality-gini-index?mapSelect=~CHN. ↑

- “IMF Board Concludes 2025 Article IV Consultation with China,” 5. ↑

- People’s Republic of China: 2024 Article IV Consultation, 3, 28, 29, and 64. ↑

- See J. Scott Davis and Brendan Kelly, “China Debt Overhang Leads to Rising Share of ‘Zombie’ Firms,” Federal Reserve Bank of Dallas, December 23, 2025. https://www.dallasfed.org/research/economics/2025/1223-davis-zombies. ↑

- Wright, “Fiscal Decay,” passim. ↑

- Octavio (Tavi) Costa (@TaviCosta), “This is wild. China’s money supply just recorded its largest annual increase on record, excluding the post-COVID stimulus period,” X, December 31, 2025, 12:28 a.m., https://x.com/tavicosta/status/2006236017981108533?s=46&t=PJbuTuaJ_cr397mT_Zf0kQ. ↑

- “US and China Money Supply: Key Differences,” Infographic Website, accessed February 2, 2025, https://infographicsite.com/infographic/us-and-china-money-supply-comparison/. ↑

- Figures calculated from the 2020, 2025, and 2026 annual reports of the People’s Bank of China. See “统计数据” [Statistical data], accessed February 26, 2026 https://www.pbc.gov.cn/diaochatongjisi/116219/116319/index.html. ↑

- Sebastian Horn, Bradley C. Parks, Carmen M. Reinhart, and Christoph Trebesch, “China as an International Lender of Last Resort,” Working Paper, Kiel Institute for the World Economy, March 2023, https://www.kielinstitut.de/fileadmin/Dateiverwaltung/IfW-Publications/fis-import/f7d738e2-14df-4d2f-8a40-741762b27cf2-KWP_2244.pdf. ↑

- Sissors, “When Does China Stop Growing,” 7-8. ↑

- Brad Setser and Mark Sobel, “It’s Time for China to Let the Renminbi Appreciate Sharply,” Official Monetary and Financial Institutions Forum, November 18, 2025, https://www.omfif.org/2025/11/its-time-for-china-to-let-the-renminbi-appreciate-sharply/. ↑

- Jürgen Matthes, Yuan Undervaluation against the Euro: Unfair Cost Advantage for China?! (German Economic Institute, July 23, 2025), https://www.iwkoeln.de/fileadmin/user_upload/Studien/Report/PDF/2025/IW-Report_2025-Unterbewertung-Yuan-gegen%C3%BCber-Euro.pdf. ↑

- Cheng Zhou, “Capital Controls in China: A Necessity for Macroeconomic Stability,” Journal of Financial Stability 75 (December 2024), https://doi.org/10.1016/j.jfs.2024.101335. ↑

- Brad Setser, “China’s Currency Is Now Facing Substantial Appreciation Pressure,” Council on Foreign Relations, January 8, 2026, https://www.cfr.org/articles/chinas-currency-now-facing-substantial-appreciation-pressure. ↑

- Shum, “China’s Prosperity.” ↑

- Derek Scissors, “When Does China Stop Growing (Entirely)?” American Enterprise Institute, March 5, 2026, https://www.aei.org/research-products/report/when-does-china-stop-growing-entirely/. ↑

- Joseph Torigian, The Party’s Interests Come First: The Life of Xi Zhongxun, Father of Xi Jinping (Stanford University Press, 2025), 9–10. ↑

- These themes are explored in more depth in Thomas J. Duesterberg, China’s Economic Weakness and Challenges to the Bretton Woods System: How Should the US Respond? (Hudson Institute, November 2023), https://www.hudson.org/foreign-policy/chinas-economic-weakness-challenge-bretton-woods-system-how-should-us-respond-thomas-duesterberg . ↑

- As the world’s second-largest economic grouping, the EU is probably the most important ally for effectively pushing back against China. The current EU trade commissioner, Maroš Šefčovič, has become increasingly outspoken on the need for a strong EU response. See Finbarr Bermingham, “EU Too Slow to Act as China Rewrites Global Trade Rules, Trade Chief Sevcovic Warns,” South China Morning Post, February 25, 2026, https://www.scmp.com/news/china/article/3344517/eu-too-slow-act-china-rewrites-global-trade-rules-trade-chief-sefcovic-warns. ↑

- See Thomas J. Duesterberg, “Fentanyl Is a Growth Industry in China’s Weakening Economy,” Wall Street Journal, June 19, 2023, https://www.wsj.com/opinion/fentanyl-is-a-growth-sector-in-chinas-weakening-economy-drug-trade-crime-syndicate-overdose-daba1c2c. ↑

-

“China Steps up Scrutiny of Capital Flows as Yuan Depreciates,” Reuters, February 26, 2025,

https://www.reuters.com/markets/asia/china-steps-up-scrutiny-capital-flows-yuan-depreciates-2025-02-27/. ↑

- US Department of the Treasury, “Fact Sheet: Overview of Section 311 of the USA Patriot Act,” News Release, March 6, 2026, https://home.treasury.gov/news/press-releases/tg1056. ↑

- Two recent books by China scholars explore in great depth the possible faltering of the current economic model and the strength of Xi’s grip on what is often called, somewhat anachronistically, the mandate of heaven. The books were the subject of a review essay by Andrew Nathan in a recent issue of Foreign Affairs. According to Nathan, both scholars suggest, based on sophisticated survey data, that there are some serious structural problems in the Chinese economy that help feed a loss of confidence and support from the Chinese people. See Andrew Nathan, “China’s Fragile Future: How Secure Is the CCP?,” Foreign Affairs, March/April 2026, 152–58, https://www.foreignaffairs.com/reviews/chinas-fragile-future-nathan. ↑